In Switzerland, dental care is almost entirely the patient’s financial responsibility. Unlike general medicine, mandatory health insurance (LAMal) only covers dental treatment in very specific and exceptional situations. This feature of the Swiss healthcare system often surprises new residents and remains poorly understood even by long-standing patients.

Understanding what is reimbursed, by which insurance, and under what conditions helps you anticipate costs, choose suitable supplementary coverage and, in some cases, obtain coverage that might otherwise be missed due to lack of awareness. This article reviews the legal framework, supplementary insurance, special cases (accidents, children, IV, supplementary benefits) and practical ways to reduce the cost of your care.

Table of Contents

Why is dental care so poorly reimbursed in Switzerland?

The Swiss system is based on a clear principle: oral health is considered an individual responsibility, largely dependent on daily hygiene and regular check-ups. LAMal, adopted in 1994, maintained this logic by including dental care in mandatory coverage only for serious conditions that cannot be avoided through reasonable prevention.

In practical terms, this means that a cavity, scaling, a crown or orthodontic treatment is not covered by basic insurance, regardless of your insurer. This rule applies to all residents, regardless of income, with the exception of a few social schemes that we detail below.

This model places Switzerland among the European countries where the share of dental care paid directly by the patient is highest. It makes choosing good supplementary insurance—and maintaining rigorous oral hygiene—all the more important to limit the need for restorative care.

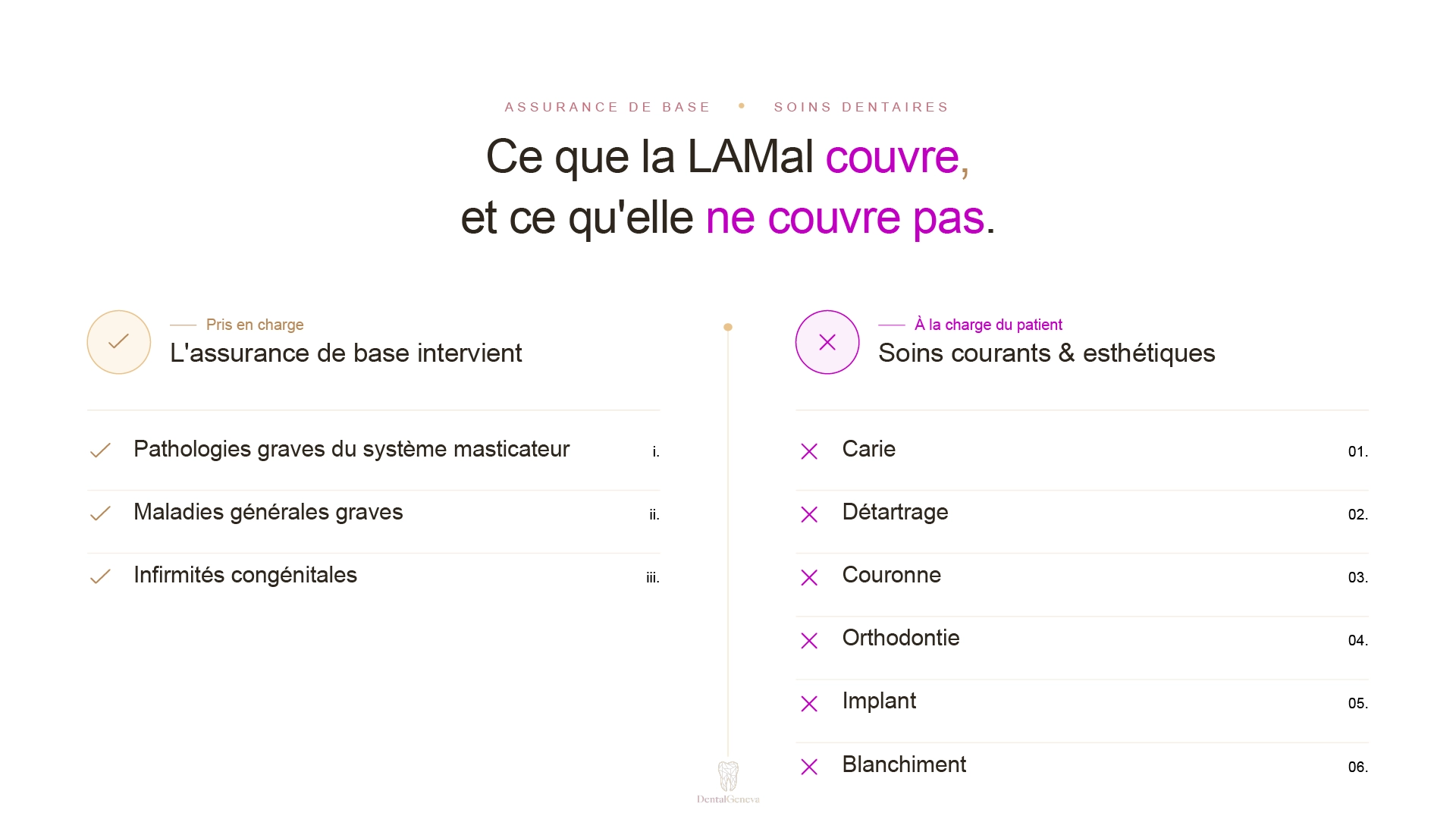

What LAMal actually reimburses

Article 31 of LAMal defines three situations in which mandatory insurance covers dental care. The technical details are set out in Articles 17 to 19a of OPAS (Ordinance on Health Insurance Benefits).

Serious and non-preventable disease of the masticatory system

These include conditions such as certain forms of early aggressive periodontitis, jaw tumours, cysts, or severe dysfunction of the temporomandibular joint. OPAS lists 18 specific diseases. Coverage is not automatic: a treatment plan must be submitted to your insurer before care begins, except in emergencies.

Serious general illness or its after-effects

When dental care is required due to another condition (leukaemia, chemotherapy or radiotherapy to the oro-facial region, certain immunosuppressive treatments, end-stage renal failure, etc.), LAMal may cover it. OPAS lists around twenty situations.

Congenital defects and consequences of accidents

Article 19a OPAS governs coverage for dental care related to a congenital defect. For accidents, coverage generally falls under accident insurance (LAA), not LAMal. We return to this below.

What is never covered by LAMal

In practice, basic insurance does not cover any of the most common dental treatments. The following are never reimbursed: scaling and professional cleaning, cavity treatment and fillings, crowns, bridges and dentures, implants, orthodontic treatment for children and adults, whitening, annual check-ups, or even the extraction of an uncomplicated wisdom tooth.

For the vast majority of patients, routine dental care therefore falls either under out-of-pocket payment or optional supplementary insurance.

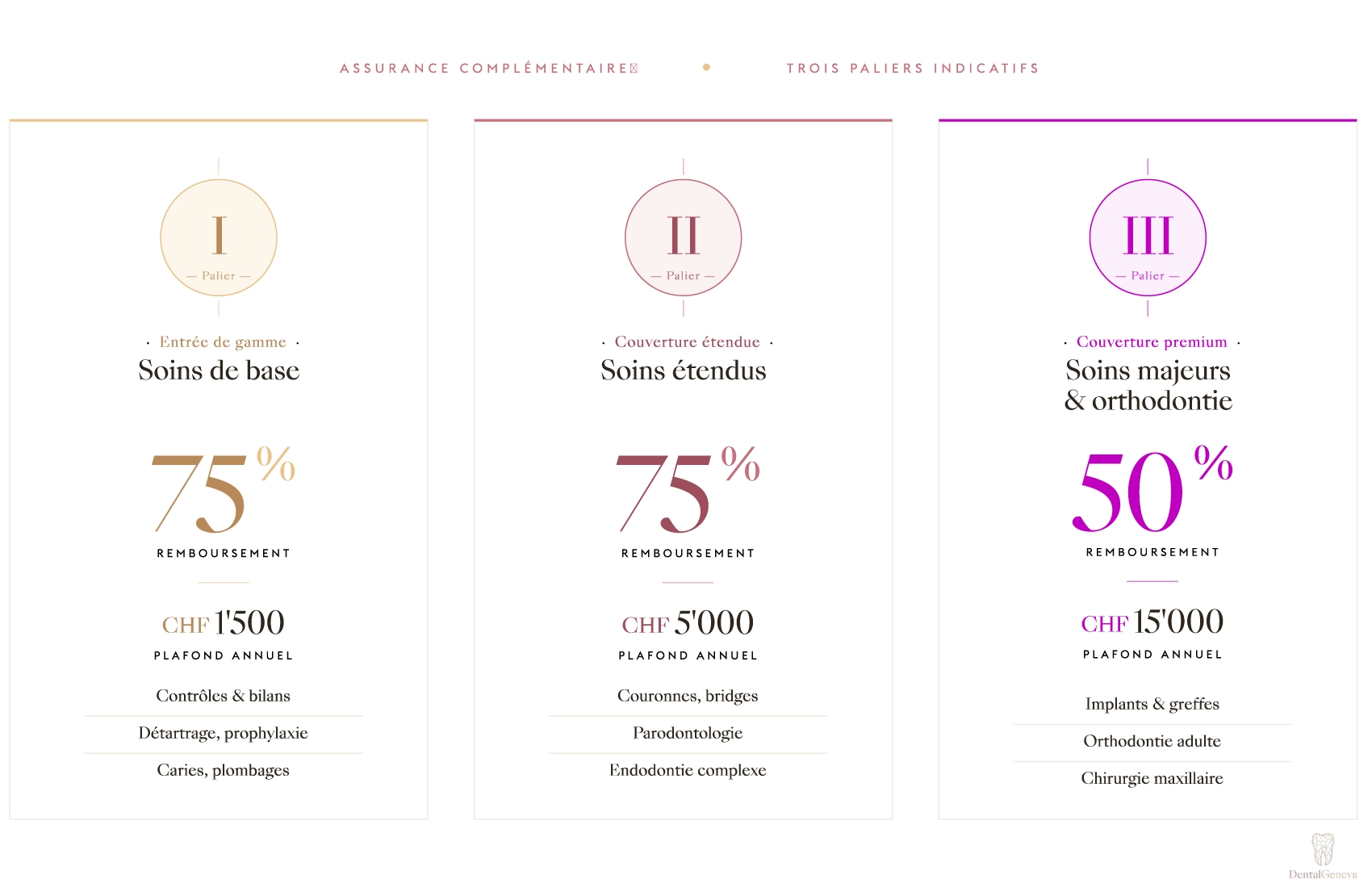

Supplementary dental insurance: understand and choose

Supplementary dental insurance is governed by the Insurance Contract Act (ICA). It is optional; its premium depends on your age, your oral health at the time you take out the policy, and the level of coverage chosen.

Types of coverage

Policies are generally divided into three categories:

- Basic care: scaling, fillings, cavity treatment, simple extractions. Typical coverage between 50% and 75%, with an annual cap often between CHF 1,000 and CHF 3,000.

- Extended care: adds periodontology, endodontics (root canal treatment), and certain fixed prostheses. Higher annual caps.

- Major care and orthodontics: crowns, implants, orthodontic treatment (especially for children). This level often requires a detailed medical declaration and imposes a waiting period.

For adult orthodontics specifically, eligibility conditions deserve careful review: we detail them in our article on supplementary insurance for adult orthodontics.

Selection criteria

Before taking out a policy, always check:

- The reimbursement percentage and the annual cap

- Waiting periods (often 3 to 12 months for routine care, up to 24 months for orthodontics)

- Exclusions (ongoing treatment, pre-existing conditions)

- Any reduction of caps after several claim-free years

- The option to take out orthodontic coverage for your children before the age limit (often 3 to 5 years)

The right time to take out a policy

Taking out coverage when you are young and in good oral health is the most effective lever. Once a condition has been declared or treatment has started, the insurer may refuse coverage or apply exclusions. For a child, planning ahead before the first cavity or the onset of a malocclusion makes it possible to obtain orthodontic coverage without exclusions.

Special cases: accidents, children, IV and supplementary benefits

Dental accidents

If you lose or break a tooth in an accident, it is accident insurance (LAA for employees, or the accident cover included in your LAMal for non-employees) that covers the treatment, provided the accident is reported promptly and documented. Coverage may include a crown, an implant, or even a denture, depending on the nature of the injuries. The report to your employer or insurer must be made without delay to avoid a refusal.

Children’s dental care in Geneva

In Geneva, the School Dental Service (SDS) provides a free annual screening at school up to 8P, as well as access to basic care at income-adjusted rates for children and adolescents aged 0 to 18. It is a useful social safety net for routine care and urgent situations.

However, follow-up in a private practice meets a different need: continuity with a practitioner who knows the child, and early detection of growth issues and malocclusions. Between ages 6 and 11, interceptive orthodontics is most effective, well before problems become visible. Supplementary dental insurance with an orthodontics component taken out early can cover a significant share. The article should baby teeth be treated? explains why this care, even when not reimbursed by LAMal, influences the development of the adult dentition.

IV, OASI and supplementary benefits

Invalidity Insurance (IV) may cover certain dental treatments related to a recognised congenital defect. Supplementary benefits (PC) paid to OASI or IV beneficiaries on low incomes may reimburse routine or essential dental care (extractions, dentures), upon submission of a quote and a prior application. Contact the cantonal compensation office to find out the exact procedures in Geneva.

Cross-border commuters and foreign residents

Cross-border commuters insured under LAMal follow the same rules as Swiss residents. Those who have chosen the right of option (CMU in France) must refer to the terms of their French insurance. Expats insured through international coverage should check dental benefits in their policy terms, which vary considerably from one contract to another.

Practical tips to reduce the bill

Always request a detailed quote

For any treatment costing more than around CHF 500, request a written quote. It allows you to compare practitioners, submit a coverage request to your supplementary insurer, and review each proposed procedure line by line. At DentalGeneva, a detailed quote is provided before any treatment that commits you, so you have time to decide.

Dr. Daniil Klimovich

Orthodontist, practice director. DentalGeneva, central Geneva.

Prioritise prevention

A scaling every 6 to 12 months costs between CHF 120 and CHF 250, while a full periodontal treatment can reach several thousand francs. The gap is even greater for cavities: a filling for an early cavity costs a fraction of a root canal treatment followed by a crown. The articles 10 golden rules of oral hygiene and when and how to use dental floss summarise the habits that make a long-term difference. Regular professional in-practice cleaning is a useful complement to daily brushing.

Seek a second opinion for major treatments

For treatment exceeding CHF 3,000 or CHF 5,000 (implants, an adult orthodontic plan, prosthetic rehabilitation), a second opinion is legitimate. It helps confirm the indication, explore less invasive and sometimes less costly alternatives, and compare technical approaches.

Spread treatment over several tax years

When medically possible, spreading treatment over two calendar years allows you to use two annual supplementary insurance caps instead of one. Discuss this option with your dentist during planning.

Deduct dental expenses from your taxes

In the canton of Geneva as well as at the federal level, unreimbursed medical expenses, including dental care, can be deducted from taxable income if they exceed a threshold (generally 5% of net income). Keep all your invoices.

Compare supplementary policies each year

The supplementary insurance market is changing. Priminfo, while useful for basic insurance, does not cover supplementary plans; for the latter, use a supplementary insurance comparator or an independent broker. Be careful, however: a change often requires a new health declaration, so it should only be considered if your oral health situation is stable.

When should you see your dentist in Geneva?

An annual check-up remains the simplest way to limit the overall cost of your oral health. Conditions detected early are treated quickly and at lower cost, while postponed care often becomes more complex and more expensive. This is even more true in Switzerland, where almost the entire bill remains your responsibility.

If you have questions about the cost of treatment, possible coverage by your supplementary insurance, or if you are unsure about whether a procedure is indicated, a consultation at the practice can help clarify matters. The practice provides a written quote before any treatment that commits you and supports patients with insurance coverage procedures when relevant.

Make an appointment with Dr Daniil Klimovich for a dental check-up and a treatment plan tailored to your situation.